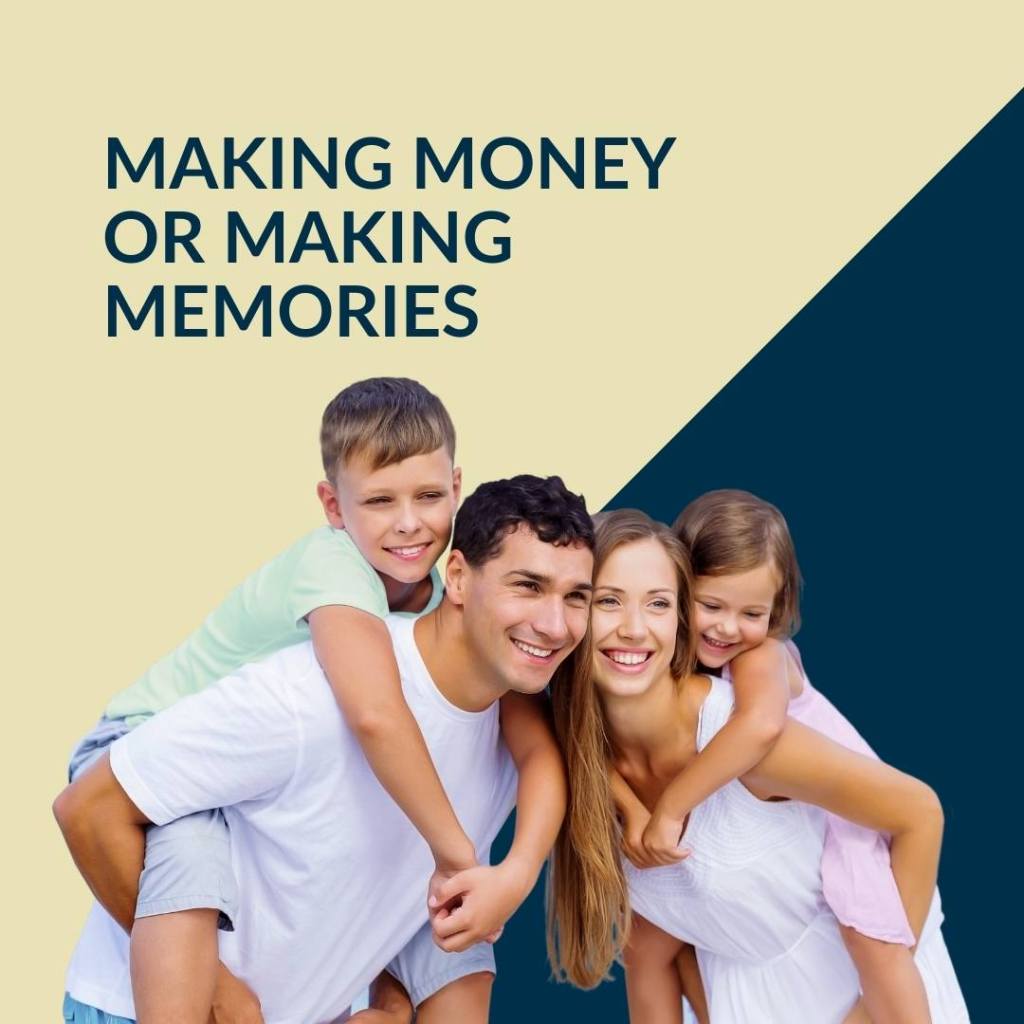

What is it you plan to do with your one wild and precious life? : How to Spend Your Life, Not Just Your Money

Introduction: The Biggest Financial Lie You’ve Been Told

Imagine reaching the final moments of your life, looking back at decades of hard work, diligent saving, and responsible financial planning—only to realize you never truly lived. Your bank account is full, but your heart is empty. The best years of your life were spent accumulating, not experiencing. The wealth you built, meant to give you freedom, ended up becoming the chains that kept you from truly enjoying the ride.

Bill Perkins, a maverick hedge fund manager, risk-taker, and adventurer, wrote ‘Die With Zero’ to challenge the greatest financial myth of all time: that success lies in amassing wealth for an uncertain future. He argues that we have it all backward. Instead of merely earning and saving, we should be maximizing our life experiences, crafting unforgettable memories, and embracing the full adventure of being alive. Money, Perkins insists, is a tool—not the end goal. Die with Zero is not just a financial strategy—it’s a call to arms against a life of regret. The ultimate goal? To leave this world not as a hoarder of wealth but as a collector of moments, having squeezed every ounce of joy, love, and adventure from our fleeting existence.

Let’s dive into the nine rules recommended by Perkins that will reshape the way you think about money, time, and what it truly means to live.

Rule 1: Wealth is Measured in Memories, Not Money

The world has conditioned us to believe that success is measured by the weight of our wallets, the size of our houses, and the brand names stitched onto our clothes. Society often equates prosperity with accumulation—more money, more possessions, more symbols of status. But beneath this relentless pursuit of material wealth, an essential truth gets buried: no matter how much we own, we cannot take any of it with us when we leave this world.

Poet Mary Oliver, in her timeless question, urges us to pause and reflect: “Tell me, what is it you plan to do with your one wild and precious life?” This is not just a poetic sentiment; it is a profound challenge to the way we think about our existence. Are we spending our lives accumulating things, or are we crafting a life rich in experiences, in stories worth telling, in moments that make our hearts race and our souls feel alive? Bill Perkins takes this challenge a step further. He insists that life is not measured by the amount of wealth we amass but by the depth of the experiences we collect. Money, after all, is a means to an end, not the end itself. When we reach our final days, we will not reminisce about our bank balances, the cars we drove, or the expensive furniture we bought. Instead, we will recall the moments that defined us—the laughter shared on a long road trip, the thrill of watching a sunset from a mountaintop, the electric energy of a concert where we sang our hearts out, the warmth of a spontaneous hug from a loved one.

The Currency of Life: Memory Dividends

Perkins introduces the concept of Memory Dividends, a powerful way to think about how experiences compound in value over time. Unlike material possessions, which inevitably depreciate, experiences appreciate. The joy they bring does not fade—it grows. Every time we recall a cherished experience, we relive it. The emotions, the details, the way we felt in that moment—everything comes rushing back, bringing us joy over and over again.

Think about your own life. What are the moments that bring a smile to your face even years later? Was it the thrill of your first solo adventure, navigating a foreign city with nothing but curiosity and courage? Was it the night you and your childhood friends stayed up talking until sunrise, knowing life would never feel quite the same again? Was it the time you stood in front of a breathtaking landscape, feeling utterly insignificant yet completely at peace?

Now compare that to the material things you once obsessed over. The phone you bought five years ago—do you even remember how excited you were when you first held it? The expensive suit or dress you splurged on—does it still hold the same magic, or has it been replaced by the next “must-have” item? The difference is striking. While material possessions lose their luster, experiences have a compounding effect. They create stories, and stories are what make a life well-lived. The more we invest in meaningful experiences, the more memory dividends we collect—memories that pay us back in happiness and fulfillment for the rest of our lives.

The Illusion of Ownership vs. The Reality of Experience

A common trap people fall into is believing that possessions define their success. We work longer hours to afford a bigger house, a newer car, or designer clothes. But often, these things serve as external validations rather than internal sources of joy. The pursuit of material wealth can be an endless treadmill—no matter how much we acquire, there is always something new to desire. Experiences, on the other hand, offer a different kind of wealth—one that is deeply personal and uniquely fulfilling. They shape who we are. Traveling to a new country expands our perspective. Learning a new skill challenges and enriches us. Spending time with loved ones strengthens our emotional bonds. These moments become part of our identity in a way that no luxury item ever could.

Perkins’ philosophy is a wake-up call. He urges us to shift our priorities—now. Instead of working tirelessly to afford more things, we should be designing a life full of extraordinary moments. This doesn’t mean being reckless with money; it means using it wisely—as a tool to create experiences that will continue to bring us joy long after the moment has passed.

How to Start Investing in Memory Dividends Today

- Identify the experiences that truly matter to you. Make a list of things you’ve always wanted to do—travel to a certain place, learn an instrument, attend a special event, or simply spend more time with the people who matter most.

- Prioritize experiences over possessions. The next time you consider making a big purchase, ask yourself: will this bring lasting happiness? Or would that money be better spent on an experience that will create memories for a lifetime?

- Capture and share your experiences. Take photos, write in a journal, or tell stories about the moments that shaped you. The more you revisit these memories, the richer they become.

How to Start Investing in Experiences Now

- Write your “Life List”—not just a bucket list, but a roadmap of what you truly want to do before time steals the chance.

- Prioritize experiences over stuff. Science shows that the joy of experiences lasts much longer than the thrill of material possessions.

- Start living your dream life today—not when you retire, not “someday,” but now.

Rule 2: The Best Time to Live Is Now

Waiting is a disease—one of the most insidious and destructive forces in a person’s life. It operates silently, convincing us that later is the right time to pursue our dreams, that someday we will travel, learn, create, explore, and live fully. But that day never arrives. Life keeps throwing obstacles, responsibilities pile up, and before we know it, we have spent our best years preparing to live instead of actually living.

Bill Perkins warns against the greatest regret of all: postponing joy. He insists that we must take hold of our experiences now—not when we’re older, richer, or when everything is “perfect.” Because the truth is, perfection is an illusion. There will never be a perfect time. There will always be bills to pay, responsibilities to manage, and unexpected setbacks. If we keep waiting for the ideal conditions, we risk waking up one day to the harsh reality that we ran out of time.

The Ancient Wisdom of Living in the Now

This is not just modern financial advice—it is ancient wisdom echoed by some of history’s greatest minds. The Stoics, the Sufis, the Zen masters, and the poets have all told us the same thing: Life is uncertain. No one is promised old age. Marcus Aurelius, the great Stoic philosopher and Roman emperor, urged people to stop delaying and start living: “You could leave life right now. Let that determine what you do and say and think.” This is not meant to be a morbid thought—it is meant to wake us up. Similarly, Rumi, the great Persian poet and Sufi mystic, wrote:

“Don’t grieve. Anything you lose comes in another form.

Don’t wait any longer. Dive in the ocean,

Leave and let the sea be you.”

Both of these thinkers, separated by centuries and cultures, point to the same truth: Your life is happening right now, and every moment you wait is a moment lost forever.

The Great Irony of Delayed Gratification

We live in a world that celebrates delayed gratification. We are taught that if we just work hard, save, and sacrifice, we will be able to enjoy life later. But Perkins challenges this idea. He argues that while some level of financial responsibility is necessary, most people take it to the extreme. How many people do you know who worked tirelessly for retirement, only to find that their health, energy, and enthusiasm were no longer what they once were? Some reach retirement and find that they no longer want to do the things they once dreamed of. Others fall sick before they ever get the chance. The brutal reality is that later is never guaranteed. This is not an argument for reckless spending. It is an argument for timely living. There are some experiences that have an expiration date—not because they are unavailable later, but because their joy and impact diminish with age.

How to Break Free from the “Someday” Trap

- Identify Experiences That Require Youth and Health

Some things simply can’t wait. Climbing Machu Picchu, learning to surf, dancing all night at a music festival, running a marathon, playing tag with your kids—these are experiences that require youthful energy. If you push them too far into the future, you may find that your body, enthusiasm, or circumstances no longer allow them. Perkins suggests making a list of “time-sensitive” experiences and prioritizing them accordingly. If something requires youth, strength, or flexibility, do it now.

- Avoid the “Save Now, Live Later” Trap

The traditional financial model tells us to work hard now and enjoy life later. The problem? Later is unpredictable. A powerful real-world example is seen in retirees who spent decades saving, only to find themselves too tired or ill to travel, too risk-averse to start something new, or too set in their ways to enjoy a radically different lifestyle. Their wealth sits unused while their spirit fades. Instead of blindly following this model, Perkins suggests a balanced approach: Don’t save for the future at the cost of your present happiness. Spend wisely, but make sure you are actively creating meaningful experiences along the way.

- Act on Your Dreams—Now

This is the golden rule: If you have the resources now, use them. If you have the money and time today to do something that has been sitting in your heart for years, do it. Waiting for the “right moment” is a trick our minds play on us. There will always be something in the way—a project at work, a financial commitment, a personal obligation. But if you truly examine these obstacles, you’ll find that most of them are just excuses. The truth is, we are afraid of fully living.

That trip to Italy? Book it.

That book you’ve always wanted to write? Start now.

That dance class? Sign up today.

That person you’ve wanted to reconnect with? Call them now.

At the end of your life, you won’t regret the experiences you had—you’ll regret the ones you didn’t.

Imagine your future self looking back at you today. What would they say? Would they thank you for taking risks, for prioritizing joy, for filling your life with adventure and love? Or would they feel sorrow for all the experiences you let slip away? Perkins reminds us that life is fleeting, and the biggest financial mistake is not overspending—it’s under-living. The truth is simple: There is no perfect time. There is only now. So start living today.

How to Break Free from the “Someday” Trap

- Identify experiences that require youth and health. Hiking in the Andes? Learning to surf? Playing with your kids? Some things can’t wait.

- Avoid the ‘save now, live later’ trap. Most people work hard for retirement, only to find their energy and enthusiasm depleted.

- Act on your dreams. If you have the resources now, use them—because time is the one thing you can never earn back.

Rule 3: Die With Zero—Not With Regret

What if, instead of making wealth accumulation our ultimate goal, we focused on using our money meaningfully throughout our lifetime? What if we saw money not as something to be hoarded but as something to be strategically spent, invested, and shared to maximize the richness of our lives? Bill Perkins turns the conventional wisdom of financial planning on its head by asking a radical yet liberating question: What is the point of dying with a fortune you never got to enjoy? Society has conditioned us to believe that financial success means accumulating as much wealth as possible, but Perkins argues that unspent money at the end of life is not a mark of discipline—it is a tragic sign of wasted time, lost opportunities, and experiences never lived.

This is not an invitation to reckless spending. Instead, it is a call to use money as it was meant to be used: to create, to experience, to connect, and to bring fulfillment—not just to ourselves but to the people we love and the causes we care about.

The Money Paradox: More Is Not Always Better

In today’s world, wealth accumulation is often mistaken for life fulfillment. Many people work tirelessly, believing that more money will automatically lead to more happiness. But research on happiness economics suggests otherwise. Beyond a certain point—where basic needs, security, and comfort are met—additional wealth does little to improve overall well-being. In fact, it can even become a burden.

Imagine a person who spends their entire career accumulating wealth, denying themselves simple pleasures, skipping vacations, and postponing joy, all in the name of financial security. Then, they retire at 70 with millions in the bank—but with failing health, diminished energy, and little time left to enjoy the life they sacrificed so much for. What was it all for? Perkins reminds us that money’s value is not in having it but in using it—wisely, intentionally, and at the right time.

Reclaiming the True Purpose of Money

- View Money as a Tool for Living, Not Just for Surviving

Most people spend their entire lives accumulating money with a survival mindset—focusing solely on financial security, preparing for worst-case scenarios, and fearing financial ruin. While responsible saving is important, Perkins encourages us to ask: What am I actually saving for? If all your needs are met and you are financially secure, yet you continue to stockpile money without using it to enrich your life, then you are treating money as an end goal rather than as a means to a fulfilling life.

Money is like stored energy—it holds potential, but if it is never put to use, it serves no real purpose. A battery left in storage eventually loses its charge; wealth that is never used similarly loses its true power. The goal should not be to die with the highest net worth but to ensure that every dollar you earn contributes to a life well-lived. Instead of asking, How much money can I accumulate?, shift the question to:

- How can I use my money to create meaningful experiences?

- How can I invest in relationships, personal growth, and joy?

- How can I ensure that my money serves my life rather than the other way around?

- Aim for Financial Security—But Not at the Cost of Your Best Years

Many people adopt an extreme approach to financial security, sacrificing their best years in pursuit of an ever-growing nest egg. The problem with this mindset is that it often postpones life indefinitely. Financial stability is crucial, but Perkins warns against over-saving at the expense of experiencing life. After all, what is the point of saving millions for retirement if, by the time you get there, your health, mobility, or desire for adventure has faded? There is a sweet spot—a balance between saving responsibly and spending wisely while you can still fully enjoy what life has to offer. Here’s a reality check:

The best time to travel freely is usually in your 30s or 40s—not your 80s.

The best time to experience physical adventure is when your body is still strong.

The best time to create lasting family memories is while your children are young.

Every life stage offers unique opportunities, but those opportunities have expiration dates. If you keep waiting, you may miss them forever. The key is to secure your financial future without postponing your life in the process.

- Set a “Spending Plan” to Ensure Your Wealth is Being Used for Joy, Not Just Hoarded

Most financial planning focuses on earning and saving, but few people have a strategy for spending their wealth wisely. Without a conscious spending plan, many people fall into the trap of accumulating money indefinitely, never knowing when it’s “enough.” Perkins recommends creating a deliberate spending plan—one that ensures your money is being used at the right time for the right things. This plan should include:

- Experiential Investments – Allocate money for things that bring joy and lasting memories: travel, hobbies, personal growth, and quality time with loved ones.

- Time-Bound Spending – Recognize that some expenses should happen earlier in life. For example, traveling in your 30s may be more fulfilling than in your 70s.

- Strategic Giving – Plan to give to family and charity at times when the money will have the greatest impact. Giving money to your children in their 20s or 30s may be far more valuable than leaving them a large inheritance when they’re already financially stable in their 60s.

- Health and Well-Being Priorities – Invest in your physical and mental well-being while it still makes a difference. Preventive healthcare, exercise, and mental wellness programs should not be afterthoughts.

Reclaiming the True Purpose of Money

- View money as a tool for living, not just for surviving.

- Aim for financial security—but not at the cost of your best years.

- Set a “spending plan” to ensure your wealth is being used for joy, not hoarded for no reason.

Rule 4: Your Money Should Outlive You—But Not By Much

One of the greatest anxieties people carry—often from childhood—is the fear of running out of money. This fear, deeply embedded in our culture, leads many to adopt extreme saving habits, constantly worrying about the future while sacrificing the joys of the present. While financial security is undeniably important, many people take it too far. They accumulate wealth obsessively, cutting corners, denying themselves experiences, and postponing joy indefinitely, all in the name of prudence. But here’s the paradox: in trying so hard to never run out of money, they run out of time. Bill Perkins challenges this traditional thinking. He argues that while financial stability is necessary, the real risk is dying with a fortune you never needed—a life half-lived in the pursuit of more, when enough would have been sufficient.

So how do you find the balance? How do you ensure you’re financially secure without hoarding money that could have been used for a richer, more fulfilling life? Perkins introduces a crucial mindset shift: optimize your wealth instead of simply accumulating it.

Many people have been conditioned to think that more money equals more security. This belief, while logical to some extent, can spiral into an unhealthy obsession with financial safety. The result? A life spent accumulating and saving without ever truly using the wealth for its intended purpose—to make life better. Psychologists call this the scarcity mindset—a state of chronic financial anxiety that convinces people they never have enough. Even millionaires can fall into this trap, believing they need just a little bit more before they can start enjoying their wealth. But how much is enough? Without an intentional strategy, enough is always just out of reach.

Signs you might be trapped in a scarcity mindset:

- You save aggressively but feel guilty when you spend.

- You delay experiences, believing you’ll have more security later.

- You check your investments obsessively, fearing market fluctuations.

- You are constantly looking for ways to cut costs—even when you don’t need to.

- You tell yourself, I’ll enjoy life when… (but that moment never comes).

This mindset is dangerous because it leads to misused wealth. Perkins’ philosophy is simple: You should enjoy your money while you’re alive, not save it all for a future that may never come. The Alternative: Optimizing, Not Hoarding. Instead of endlessly saving, Perkins advocates for wealth optimization—a strategy where you secure financial stability but actively allocate funds toward meaningful experiences. This requires a shift in mindset:

- From hoarding to purposeful spending: Instead of accumulating wealth indefinitely, create a system where your money works for you—providing financial security and funding experiences.

- From anxiety to confidence: Instead of living in fear of financial ruin, build a solid plan that ensures you have enough to live well while also enjoying your wealth.

- From delayed living to intentional enjoyment: Instead of postponing joy for retirement, integrate fulfilling experiences now, when they can have the greatest impact.

Rule 5: Give While It Matters

Most parents dream of providing financial security for their children. They work hard, save diligently, and often plan to leave behind a substantial inheritance as a final act of love. But when exactly do children need that financial support the most? Research shows that the vast majority of inheritances are received when the beneficiaries are already in their 50s or 60s—a time when they are often financially stable, nearing retirement, or at least well past the struggles of early adulthood. By then, an inheritance may serve as a comfortable bonus, but it is far less life-changing than it could have been earlier in life. Bill Perkins challenges this traditional approach. He argues that instead of waiting until death to pass down wealth, parents should consider giving earlier—when the money can have the most impact.

Why Traditional Inheritance Timing Is Flawed

The common belief is that leaving behind a large inheritance is the best way to take care of the next generation. However, this often results in misaligned timing—children inherit wealth when they are already financially independent, well into their careers, or even retired themselves. Consider these scenarios:

- A 60-year-old inherits money from their 85-year-old parent. They already own a house, have investments, and are preparing for their own retirement. The money provides comfort but doesn’t change their life trajectory.

- A 30-year-old receives financial support to buy their first home, start a business, or invest in their career. That money has the potential to transform their financial future.

The question is simple: When does money create the most value? Perkins argues that money has the highest utility in early adulthood, when people are making major life decisions—building careers, starting families, and laying the foundations for financial stability. Instead of saving money indefinitely and passing it down later in life, Perkins suggests strategic early giving—offering financial support to children when it actually makes a difference. Research suggests that between ages 26 and 35 is the most impactful time for financial assistance. At this stage in life, young adults are:

✔ Establishing their careers and often struggling with student debt.

✔ Looking to buy a home but facing rising property prices.

✔ Considering marriage, children, and family expenses.

✔ Taking calculated risks—entrepreneurship, further education, or career shifts.

Receiving financial support during these years can change their entire financial trajectory, helping them make smarter long-term decisions rather than playing catch-up later in life. The goal of early giving is not just to distribute wealth but to empower children at critical moments in life.

There’s something profoundly different about giving while you’re alive versus leaving money in a will. Perkins makes a compelling argument: Why not enjoy the impact of your generosity while you’re still here to see it?

The Same Principle Applies to Charity: Perkins extends this idea beyond family wealth: the same principle applies to charitable giving. Many people plan to leave large donations to charities in their wills, believing this to be a noble final act. But what if you could see the impact of your generosity now?

Giving to charity while alive allows you to:

✔ See tangible results from your contributions.

✔ Ensure your donations align with your values.

✔ Actively participate in causes you care about.

For example, if you are passionate about education, funding scholarships or donating to schools while you’re alive allows you to witness students benefiting from your help. If you care about healthcare, donating to medical research or hospitals in your lifetime allows you to see progress being made. Why wait for your money to make a difference after you’re gone when it can change lives today?

Rule 6: Escape the Autopilot Trap

Too many people drift through life without ever truly living. They wake up to the same alarm, follow the same morning routine, commute the same route, sit through the same meetings, return home exhausted, and repeat the cycle the next day. The script rarely changes. Life becomes a sequence of tasks—working, saving, and preparing for a future that seems distant and abstract. Days turn into weeks, weeks into years, and before they realize it, decades have slipped through their fingers. Their youth is gone, their health is fading, and they suddenly wonder where all the time went.

Bill Perkins urges us to snap out of it—to wake up before we sleepwalk through life’s most precious moments. He warns against falling into the dangerous trap of autopilot living, where our routines become so ingrained that we stop questioning whether they actually bring us joy or fulfillment. Too many people live as if they are rehearsing for a future where they will finally be free to enjoy themselves. But when does that moment arrive?

For some, it never does. They keep waiting—until they retire, until they have more money, until they feel “ready.” But by the time they realize they’ve been postponing their happiness, it’s often too late. Their energy has dwindled, their opportunities have passed, and the adventures they once dreamed of now seem impossible. Perkins’ message is clear: Wake up now. If you’re just moving through life mechanically, it’s time to take control. Start asking yourself: Am I truly living, or am I just existing? Am I making the most of my time, or am I just filling it with obligations? Life isn’t something to be endured—it’s something to be designed, crafted, and lived with intention. The danger of living on autopilot is that it creates an illusion of permanence. It makes us believe we have all the time in the world. But time is slipping away every second, and the only way to truly make the most of it is to wake up and live deliberately—before life makes the choice for you.

How to Live Intentionally

- Conduct a life audit. Are you living, or just existing?

- Identify habits that steal your joy and replace them with conscious, fulfilling actions.

- Make every day count—because each one is a page in the book of your life.

Rule 7: Time Buckets—Because Life Comes in Seasons

Life is not a single, continuous journey—it unfolds in seasons, each offering its own unique set of opportunities, challenges, and experiences. Bill Perkins introduces a powerful concept called “time bucketing,” a way of recognizing that different phases of life come with different priorities, and that planning our experiences accordingly ensures we don’t miss out on the things that truly matter. Imagine your life as a series of distinct chapters, rather than one long stretch of time. Each phase—your 20s, 30s, 40s, and beyond—has its own energy, desires, and possibilities. The things you can do in your 20s, like backpacking through Europe on a shoestring budget, staying out all night at music festivals, or taking bold career risks, may not be as easy or appealing in your 50s or 60s. Similarly, the joy of raising children, nurturing relationships, and focusing on deep personal growth may be best suited for middle age, while the later years of life might be about reflection, mentorship, and legacy. Perkins urges us to recognize that time is not an unlimited resource. If we don’t deliberately plan for experiences in the right phase of life, we risk missing them entirely. Too many people assume they can always “do it later,” without realizing that later might not be as accommodating as they think. There is a window for everything—physical adventures, career shifts, family milestones, and even personal development.

Time bucketing is a proactive approach to life design. Perkins suggests creating a timeline of your life, dividing it into decade-based buckets, and assigning key experiences to each one. For example, if traveling the world is important to you, when will you do it? If learning a new skill, writing a book, or starting a business is on your wish list, when will you prioritize it? This exercise forces you to be intentional about your time, ensuring that you don’t reach the later stages of life with a long list of “I wish I hads.”

By embracing this mindset, you stop deferring happiness and start aligning your actions with what truly matters in each season. Instead of letting time slip away unnoticed, you create a life by design, ensuring that every stage is filled with meaningful, fulfilling experiences suited to that particular moment in life.

How to Use the Time Bucket Method

- Create a timeline of your life, divided into decades.

- List experiences best suited for each stage.

- Act on them at the right time—before the window closes.

Rule 8: Know When to Stop Chasing Wealth

At some point in life, everyone reaches their peak net worth—the moment when their financial resources are at their highest. Bill Perkins argues that once we hit this point, our focus should shift from accumulating more wealth to spending it intentionally on experiences that enrich our lives. After all, what is the point of amassing more money than we can realistically use? Past a certain threshold, accumulating wealth stops adding to our happiness and instead becomes an abstract number in a bank account—one that holds no real meaning unless put to use. For most people, peak net worth occurs in midlife—typically between the ages of 45 and 60. By this stage, careers have matured, investments have grown, and income is at its highest. It’s a moment when financial security is often well established, but the tendency to keep accumulating just in case can become a trap. Instead of transitioning into a period of intentional enjoyment, many people continue saving excessively, driven by habit, fear, or an outdated idea that wealth equals security.

But here’s the truth Perkins wants us to grasp: Beyond a certain point, more money does not bring more happiness. Research in behavioral economics supports this claim—once basic needs, financial security, and a comfortable lifestyle are met, additional wealth contributes little to overall well-being. What does contribute? Meaningful experiences. Travel. Learning. Deep connections with loved ones. Moments that make us feel alive. The key, then, is recognizing when we reach our peak net worth and making a conscious shift from accumulation to utilization. This doesn’t mean reckless spending or throwing financial responsibility out the window—it means understanding that money is only valuable when it is used to enhance our lives. Perkins challenges us to ask: Am I still saving out of necessity, or out of habit? Am I accumulating for a future that I may not fully enjoy? Instead of hoarding money for the later years, when health and energy may decline, he encourages us to spend on experiences while we are still in our prime.

Imagine reaching your peak net worth but continuing to save aggressively, only to realize later in life that you’ve missed your best opportunities for adventure, spontaneity, and meaningful pursuits. What’s the point of waiting until retirement to travel if your energy and enthusiasm have faded? Why delay spending time with loved ones when life’s uncertainties make the future unpredictable? The message is clear: Money is not the goal—life is. Once we reach a financial position where our needs are covered, it is time to start reaping the rewards of our hard work, not just stockpiling them. Whether it’s taking that dream trip, investing in personal growth, or creating unforgettable experiences with family and friends, spending wisely on experiences creates the real wealth of life—joy, fulfillment, and memories that last far longer than any bank balance.

Rule 9: Be Bold When the Stakes Are Low

Fear is the greatest enemy of an extraordinary life. It whispers doubts in our ears, convinces us to stay within our comfort zones, and tricks us into believing that playing it safe is the smartest option. But as Bill Perkins reminds us, playing it safe all your life is the biggest risk of all.

The older we get, the more cautious we become. We start calculating risks differently, weighing our decisions against responsibilities, stability, and potential losses. The boldness we had in youth slowly fades as obligations pile up—family, mortgage payments, career commitments. We become risk-averse, clinging to security rather than embracing uncertainty. And before we know it, we’ve spent years avoiding failure instead of pursuing greatness.

But here’s the truth: When you’re young, you have the most freedom to take risks—and the least to lose. This is the time to start the business, take the solo trip, move to a new city, switch careers, chase an unconventional dream, or embrace uncertainty with open arms. The downside is small, but the upside is enormous.

Why Taking Risks Early in Life Matters?

Failure Is Less Costly When You’re Young: When you’re in your 20s or early 30s, setbacks are easier to recover from. If you start a business and it fails, you can start over. If you take a job abroad and it doesn’t work out, you can return home and try something new. There’s time to rebuild, pivot, and experiment. But as you get older, the stakes feel higher—financial security, family obligations, and lifestyle expectations make taking risks feel impossible.

Opportunities Shrink with Time: Every stage of life offers different possibilities, but some doors close forever if you wait too long. You may dream of backpacking across Asia, but by the time you’re in your 50s, your energy and priorities may have shifted. You may want to switch careers, but once you’re deep into a profession, breaking away becomes harder. The longer you wait, the fewer options remain.

Regret Accumulates More than Money: People often regret the risks they didn’t take more than the ones they did. Studies show that as people age, they wish they had been braver, that they had pursued their passions instead of following the safe, expected path. The greatest tragedy is realizing you never even tried.

Conclusion: Spend Your Life, Not Just Your Money

At the end of the road, no one remembers their bank balance. They remember love, laughter, adventure, and the moments that took their breath away. Die With Zero is a wake-up call: don’t wait until it’s too late. Your wealth isn’t just for saving—it’s for living. So take the trip. Make the call. Spend the money. Chase the dream. Because in the grand balance of life, the goal isn’t to die rich—it’s to die fulfilled.

Dr Mukesh Jain is a Gold Medallist engineer in Electronics and Telecommunication Engineering from MANIT Bhopal. He obtained his MBA from the prestigious management institute, the Indian Institute of Management Ahmedabad. He obtained his Master of Public Administration from the Kennedy School of Government, Harvard University along with Edward Mason Fellowship. He had the unique distinction of receiving three distinguished awards at Harvard University: The Mason Fellow award and The Lucius N. Littauer Fellow award for exemplary academic achievement, public service & potential for future leadership. He was also awarded The Raymond & Josephine Vernon award for academic distinction & significant contribution to Mason Fellowship Program. Mukesh Jain received his PhD in Strategic Management from IIT Delhi. His focus of research has been Capacity building of organizations using Positive psychology interventions, Growth mindset and Lateral Thinking etc.

Mukesh Jain joined the Indian Police Service in 1989, Madhya Pradesh cadre. As an IPS officer, he held many challenging assignments including the Superintendent of Police, Raisen and Mandsaur Districts, and Inspector General of Police, Criminal Investigation Department and Additional DGP Cybercrime, Transport Commissioner Madhya Pradesh and Special DG Police. He has also served as Joint Secretary in Ministry of Power and Ministry of Social Justice and Empowerment, Government of India. As Joint Secretary, Department of Persons with Disabilities, he conceptualized and implemented the ‘Accessible India Campaign’, launched by Hon’ble Prime Minister Shri Narendra Modi in December 2015. This campaign is aimed at creating accessibility in physical infrastructure, Transportation, and IT sectors for persons with disabilities and continues to be a flagship program of the Ministry of Social Justice and Empowerment, Government of India since 2015.

Dr. Mukesh Jain has authored many books on Public Policy and Positive Psychology. His book, ‘Excellence in Government, is a recommended reading for many public policy courses. A leading publisher published his book- “A Happier You: Strategies to achieve peak joy in work and life using science of Happiness”, which received book of the year award in 2022. His other books are : ‘Mindset for Success and Happiness’, ‘Seeds of Happiness’, and ‘What they don’t teach you at IITs and IIMs’.

He is a visiting faculty to many business schools and reputed training institutes. He is an expert trainer of “The Science of happiness”. He has conducted more than 250 workshops on the Science of Happiness at many prominent B-schools and administrative training institutes of India, including Indian School of Business Hyderabad/ Mohali, National Police Academy, IIFM, National Productivity Council etc.

Leave a reply to Nivedita Ashish Cancel reply